Here's the Proof that Banking Crises Simply Don't Need to Happen. Period.

I recently watched a discussion between an academic and a central banker that exposed the kind of intergenerational amnesia that is undermining financial stability and our economy.

The presentation was by Moritz Schularick, an economist I deeply respect for having stewarded the compilation of some of the first multi-country and multi-century economic datasets that include data points on banking crises and bank money creation.

Dear reader: If hearing “banking crises” doesn’t put your nervous system on high alert, you may not be aware of Moritz’s earlier work showing that bank-led credit crises trigger our most destructive economic crises. Economic recessions caused by bank lending booms and busts have longer and deeper periods of unemployment, more business bankruptcies, and worse debt crises for households, businesses, and governments (when compared to recessions caused by natural disasters, wars, etc). So, if you dislike living through economic crises, you should be very concerned about banking crises!

In his talk, Schularick explained how he and his team had analyzed dozens of banking crises in seventeen countries over a 140 year period.

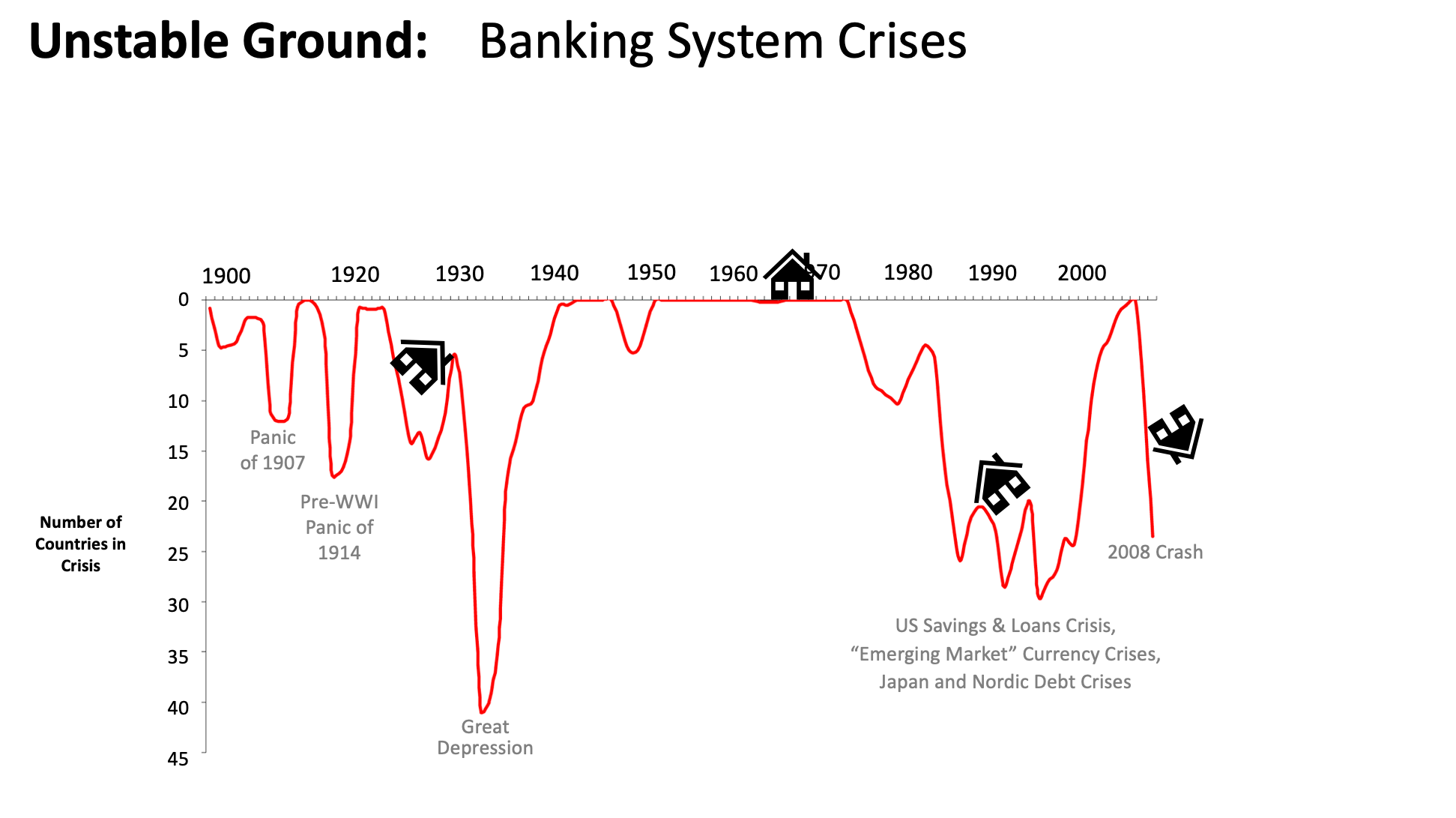

During his talk, Schularick showed the following chart detailing all the banking crises that have taken place since 1870 in seventeen countries, which I’ve re-created to remove distracting text:

After speaking about all the things his team had learned by studying central banks’ responses to each of the banking crises, Schularick received a question from a leading economist for the Bank of France:

“On the table there was almost nothing between 1930 and 1990. There is a big chunk in the table which is blank. So I was wondering: Is it true that there were no banking or financial crises at that time?”

- Bussiére Matthieu, Phd, Director of the Directorate, Economics and International and European Relations, Banque de France

Now, just to put Matthieu’s comment in perspective, you need to understand that the Bank of France is the central bank of France. As the bank’s director of economics and international relations, Matthieu is an active participant in international negotiations about how the Euro currency is managed by the European Central Bank. He also is involved in decisions about how European central banks regulate the banks in their countries to ensure stability.

It would be reasonable to think that someone in Matthieu’s role would be aware of previous eras of highly stable banking. In fact, you would think that he would be studying such eras carefully for lessons to apply today.

Staggeringly, Matthieu’s question for Schularick revealed that he was completely unaware of the period in the middle of the last century when there wasn’t a single banking crisis in 17 countries for a period that ranged between 30 and 50 years, depending on the country.

If Matthieu was not aware of this “oasis of calm,” as Schularick’s team dubs it, it is safe to assume that many of the other central bankers participating alongside Matthieu in high-level monetary policy and bank regulation conversations in the EU area also unaware. If today’s monetary and banking regulatory leaders are aware, they should be having urgent conversations about why their leadership is completely failing to match the perfect stability achieved by a previous generation of leaders between 1940 and 1970. But there is no evidence of that conversation, that I have seen.

A previous generation of central banking leaders figured out how to not have any banking crises, at all, for thirty straight years. Today’s central bankers have forgotten what they knew.

This is stunning for a lot of reasons

As Schularick pointed out to Matthieu, his dataset isn’t the first one to highlight this wondrously tranquil period in banking history. Even before the 2008 financial crisis, a team of researchers at Harvard Business School had compiled a similar dataset that covers 66 countries, which revealed the same pattern, shown here in one of their 2013 papers:

The leaders of that Harvard study, Carmen Reinhart and Kenneth Rogoff, even wrote an influential book in 2009 which identified intergenerational amnesia as a culprit in banking crises: “short term memories make it all too easy for crises to recur.” (Inexplicably, Reinhard and Rogoff write in the same paper in which they published the above chart showing 30 years of remarkable global banking stability, that “graduation from banking crises has proven, so far, virtually impossible.”)

Unfortunately, Carmen and Kenneth made some mistakes in the analysis of their dataset and came to the incorrect conclusion that government austerity is a good solution to banking and financial crises. The fact that many politicians around the globe cited their analysis when passing austerity cuts post-2008 is a devastating lesson in the dangers of drawing causal conclusions from data correlations.

Nevertheless, their analytical errors don’t change the fact that by 2009 and 2012 there were multiple highly-cited datasets shining a bright light on the 1940-1970 era as being a high-water mark in the history of banking stability, and therefore economic stability. Certainly, it was a remarkably better banking era than what came before and what we’ve experienced since.

The truth is that that banking crises are economic earthquakes that crack open the ground and swallow-up the hopes, dreams, and investments of generations.

Banking Crises vs Wellbeing

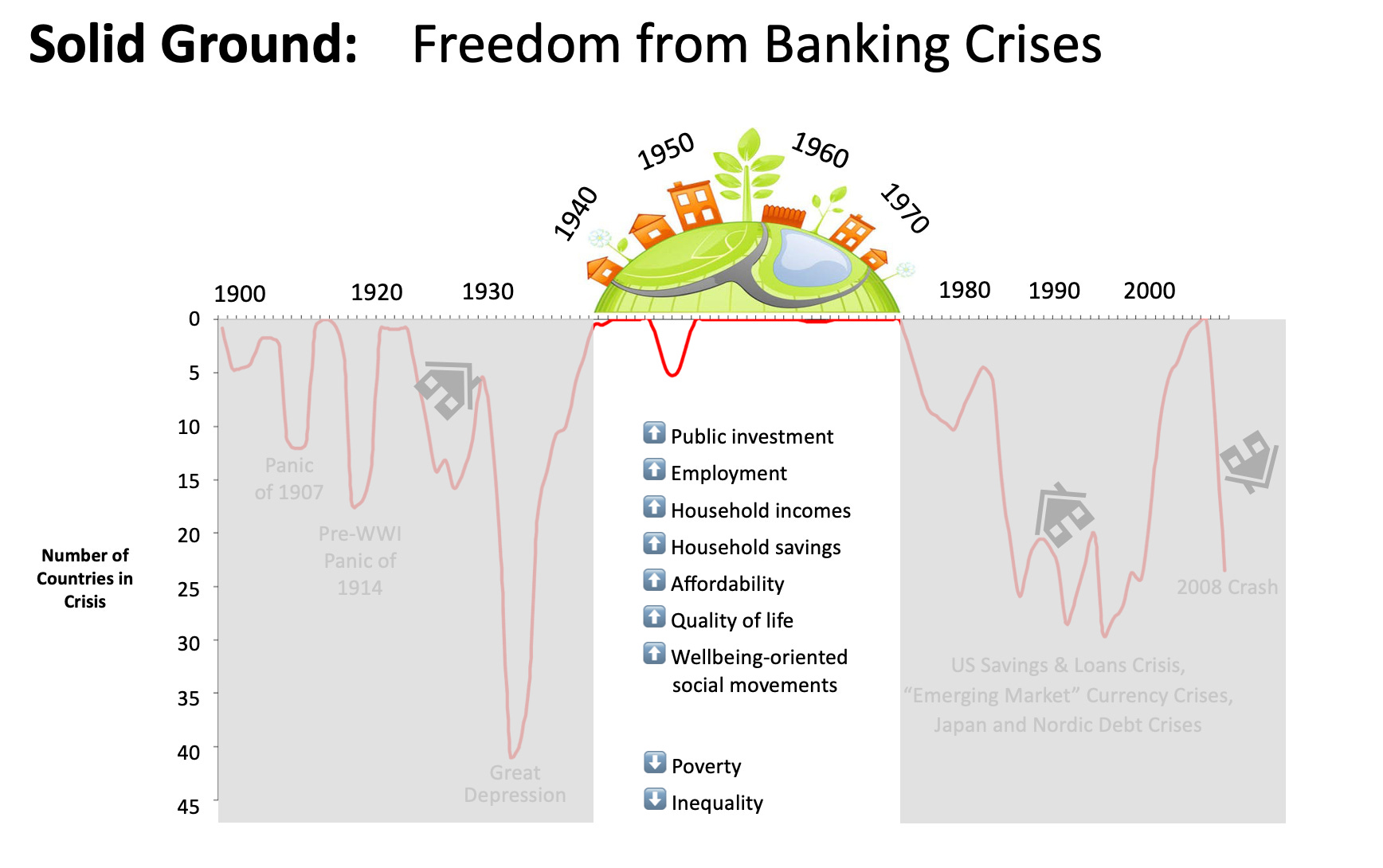

Between 1940 and 1970, the countries that had zero banking crises experienced significant increases in public investment, such as new schools and universities, affordable housing, hospitals and healthcare, parks, and more. Employment and wages rose for the working classes, creating middle classes. Household savings rose and leisure time increased. Debt levels, poverty, and inequality went down substantially.

Not all of these things were due to banking stability, of course, but they were certainly enabled by it. To put it another way, empirical data shows clearly that banking crises are devastating for all of those same economic indicators. Banking crises frequently lead to “financial recessions” which are, on average, 3 times deeper and longer than non-financial recessions in terms of productivity losses, unemployment, and business closures. They are also associated with large upswings in inequality. In fact, financial recessions have a permanently scarring effect on economies that is only rivaled by energy price shocks.

Banking crises have such a devastating effect, in part, because they result in an 86% increase in government indebtedness within 3 years, on average. This is laregely due to the fact that citizens demand their governments provide some level of a social safety net. In many countries, this comes in the form of “automatic stabilizers” that kick in whenever a crisis hits, such as unemployment insurance and anti-poverty assistance. The resulting spike in public indebtedness typically leads to severe cuts in public services and public investment. (As noted, Reinhart and Rogoff recommend such cuts as the remedy to the public debt burden caused by banking crises, instead of recommending that banking crises be abolished altogether as they were for 30-50 years in the middle of the last century.)

Interestingly, banking crises also tend to spark right-wing swings in politics that often turn authoritarian, much as we have seen around the world since 2008.

Why did only one generation get to enjoy the hard-earned discovery that banking crises are completely avoidable before the wisdom was lost??

The truth is that that banking crises are economic earthquakes that crack open the ground and swallow-up the hopes, dreams, and investments of generations. To illustrate how much of a difference it makes for societies to be able to build their communities on the solid ground of an economy that is free of banking crises, I like to flip Carmen and Kenneth’s chart upside down so that the crises appear as crevices that open up under households.

With the chart flipped like that, the flat line of the 1940-1970 era reflects what it was: stable ground on which to build a healthy society. (Or, stable ground on which to try to build a healthy society. While many social indicators improved mid-century, such as wages, savings, and reduced inequality, the era lacked social wellbeing with respect to race, gender, colonialism, etc.)

I hope that people see how much better the world can be when banking crises are abolished, as the empirical data shows is possible. I hope people even feel envious of the financial stability of that era. Maybe even get a little angry, too. Why did only one generation get to enjoy the hard-earned discovery that banking crises are completely avoidable before the wisdom was lost???

Why does a leading central bank economist not know all this?

Why are Matthieu and his colleagues in the leadership ranks of European central banks not anxiously comparing their own performance to that high-water mark era?

I’d love for someone to study that question extensively. Tracing the loss of the wisdom that guided economic leaders during the 1940s, 50s, and 60s would be a good way to learn how to stop such intergenerational amnesia in the future. But for now…

The important thing to observe is that, today, some of the economists leading our monetary systems are not aware that banking crises are completely avoidable.

In some sense, this shouldn’t come as a surprise considering how much we hear our central bankers talk about “promoting stability” instead of “permanently eliminating instability”. They simply don’t have an abolition mindset – even though history shows that abolishing banking crises is completely within our ability. Not just in theory, but in practice.

So what exactly did so many countries do at the same time to completely eliminate banking crises?

Countries took diverse pathways to achieve the same goal of ending banking crises. (The fact that today’s leaders can’t find even one pathway to completely eliminate banking crises is damning in consideration of the historical evidence that there are multiple ways that work.) At a high level, the pathways that countries took included one or more of these elements (and this is a non-exhaustive list):

The subordination of the banking sector to government-led economic development policies. There were multiple ways of doing this. A few particularly good resources on the methods governments employed are Eric Monnet’s Controlling Credit (Chapter 7), Credit Policy and the ‘Debt Shift’ by Bezemer et al., and Rebuilding Banking Law by Menand and Ricks.

Joining international monetary system agreements that obligated countries to cooperate in stabilizing exchange rates and stopping money from flowing across borders in rapid and destabilizing ways (e.g., speculative “hot money”). See “Bretton Woods agreement.”

Government regulation of interest rates to keep borrowing costs stable and low, especially for government borrowing.

The creation of new money specifically for funding government priorities (“monetary financing”)

In general, all of these measures had a common goal, which was to ensure that the legal privilege to create money was being directed into the service of public priorities and in ways that were stabilizing rather than destabilizing.

If I had to recommend one resource on the regulation of the banking sector in this era, it would be Eric Monnet’s Controlling Credit. Ironically, given Matthieu’s lack of information about this era of banking history, Monnet’s book is focused on France’s banking regulation practices. In Chapter 7, he also provides a survey of what other countries were doing at the same time.

If you want to be a banking crisis abolitionist, no one can tell you it isn’t possible. It’s been done already in dozens of countries for decades at a time!